So, you’re ready to get a home loan and face one of the first, and biggest, decisions: should you use a mortgage lender or a broker? Understanding this choice is the first step towards securing the right financing for your dream home. Understanding the mortgage lender vs broker decision helps home buyers compare loan options, interest rates and guidance when choosing the right home loan.

Think of it this way: a direct lender is like a brand-specific store. They only offer their own products. A mortgage broker, on the other hand, is like an expert personal shopper. They have access to a huge range of loans from many different lenders and work to find the perfect fit for you, promising a solution tailored to your unique financial situation.

Lender or Broker: Making Your First Big Decision

Getting a mortgage is easily one of the biggest financial moves you’ll ever make. The path you take to get there—either going straight to a bank or using a mortgage broker—can seriously shape your experience and the loan you end up with.

It’s tempting to think it’s all about chasing the lowest interest rate, but it’s much more than that. It’s about finding the right partner and the right product for your unique financial situation. Each option has its own process, its own perks, and its own potential pitfalls.

Understanding the Two Paths

Let’s stick with the shopping analogy.

Going directly to a lender is like walking into a single brand’s flagship store. You’ll get to know their product line inside and out, and if you’re already a customer, that existing relationship might even give you a leg up.

Working with a mortgage broker is more like hiring a personal stylist who knows every single shop in the city. You tell them what you need, and they hit the pavement, searching the entire market to find options you probably would have never found on your own.

Your choice between a mortgage lender and a broker really sets the stage for your entire home-buying journey. One offers a direct, single-source approach, while the other gives you broad market access and personalised guidance.

This guide will break down what each path looks like. We’ll get into who these professionals work for, how that changes the loans you see, and what it all means for your bank account in the long run. Nailing this core difference from the start puts you in the driver’s seat.

To make things even clearer, let’s look at a quick side-by-side comparison.

Mortgage Lender Vs Broker At A Glance

This table sums up the key differences at a high level, helping you see which route might align better with your needs right from the get-go.

| Feature | Mortgage Lender (Direct Bank) | Mortgage Broker |

|---|---|---|

| Loan Products | Limited to their own products only. | Offers a wide variety of loans from multiple lenders. |

| Allegiance | Works for the bank or lending institution. | Works for you, the borrower. |

| Interest Rates | Provides only their own rates. | Can compare rates across many different lenders. |

| Advice | Advice is centred around their product suite. | Offers impartial advice based on the whole market. |

| Process | You manage the application directly with the bank. | Manages the application and lender communication for you. |

As you can see, the fundamental difference comes down to choice and allegiance. A lender sells you their product, while a broker helps you shop for the best product available.

Going Direct To A Mortgage Lender

Heading straight to a mortgage lender is the old-school way, and for many people, it’s still their first port of call. A lender is the institution with the money — think big banks, credit unions, or other financial groups that actually fund your home loan.

Going direct means you’re cutting out the middleman and dealing one-on-one with the source. This can feel comfortable, especially if it’s your own bank. You already know them, they know you, and there might even be loyalty perks or package deals on the table. The process is pretty straightforward: you apply, they check you out, and they offer you a product from their shelf.

What the Lender Application Process Looks Like

When you’re dealing directly with a lender, you’re their customer, and they want to sell you one of their home loans. It’s a linear path from A to B.

- The First Chat: You’ll sit down with one of their loan officers. They’ll run through the home loans they offer and do a quick check to see if you qualify based on your income, savings, and credit score.

- The Paperwork: This is the deep dive. You’ll submit a full application with all your financial documents – payslips, bank statements, the lot.

- Underwriting: The lender’s back-office team gets to work, double-checking everything to give your loan the final yes or no.

- Settlement: Once you get the green light, they’ll handle the final steps to get the funds ready for your property purchase.

The Upsides and Downsides

The biggest advantage of going direct is simplicity. If you’re with a bank you already trust, there’s a sense of security. You have a single point of contact, and you’re dealing with a big, regulated name you recognise.

But here’s the catch: a lender can only sell you what’s on their own shelf. They can’t tell you if a competitor down the road has a sharper interest rate or a loan with more flexible features. This is the biggest drawback and a key reason the mortgage lender vs broker dynamic has shifted so much.

This lack of choice can mean missing out on a significantly better deal. Lenders offer stability, sure, but brokers bring competition to the table, and that’s almost always a win for the borrower.

The broking industry is now a major force in the Australian economy, contributing an estimated $4.1 billion in value and arranging around $353 billion in new home loans annually, showcasing its vital role in creating a more competitive lending environment. Learn more about the value of the mortgage broking industry.

For someone with a simple financial situation who values the comfort of sticking with who they know, going direct can work just fine. But if your goal is to find the absolute best deal the market has to offer, you’re only seeing a tiny slice of the pie.

Partnering With A Mortgage Broker

Now, let’s look at the other path: bringing a mortgage broker onto your team. Think of a broker as a licensed expert who acts as your personal guide, connecting you (the borrower) with a whole panel of different lenders. Their job isn’t to push one bank’s product; it’s to sift through the entire market to find the loan that’s genuinely right for you.

Here’s the key difference: a lender works for the bank, but a broker works for you. In Australia, this isn’t just a promise—it’s the law. Brokers have a legal best interests duty, meaning they must put your financial wellbeing ahead of their own or the lender’s. This completely changes the game.

The Power of Choice and Expertise

The biggest win when using a mortgage broker is access. Instead of being stuck with the handful of products one bank offers, a broker lays out dozens of home loan options from major banks, smaller credit unions, and even specialist lenders you’ve probably never heard of. This forces lenders to compete for your business, which can mean better interest rates and more flexible terms for you.

A good broker also brings years of industry know-how to the table. They live and breathe the fine print, know which lenders are friendly to certain situations (like self-employed income or a smaller deposit), and can negotiate on your behalf.

A mortgage broker does all the heavy lifting for you. They chase up the complex paperwork, deal with the lender, and walk you through every step from application to settlement. It saves a huge amount of time and stress.

This kind of hands-on support is a lifesaver for first-home buyers or anyone with a tricky financial situation who might get a “no” by going direct. If you need a clearer picture of the difference between a direct lender and a mortgage loan broker, our detailed guide breaks it all down.

How a Mortgage Broker Gets Paid

So, what’s the catch? One of the first questions people ask is about the cost. In most cases, you don’t actually pay the broker directly for their service. Instead, they receive a commission from the lender, but only after your loan is successfully settled.

This commission structure is tightly regulated to keep things transparent and fair. That “best interests duty” we mentioned legally forces them to recommend a loan that suits your needs, regardless of which lender pays them a higher commission.

It’s a model that clearly works. The mortgage broking industry has exploded in popularity, showing just how much Aussies value independent advice. As of 2025, there are now 11,521 mortgage broking businesses in Australia—a jump of 7.1% from the previous year. This growth proves that in a complicated lending market, people are voting with their feet for expert guidance. Discover more insights about the growth of mortgage brokers in Australia on ibisworld.com.

When To Choose A Lender Vs A Broker

Deciding between a mortgage lender and a broker isn’t about which one is “better” in general—it’s about which one is better for you. This is where we get practical and look at your personal situation.

Your choice really boils down to your circumstances. Are you a first-timer feeling a bit overwhelmed? Self-employed with tricky paperwork? Or an experienced investor looking for sophisticated loan structures? Each path has its pros and cons.

Let’s walk through a few common scenarios to see how it plays out in the real world.

Borrower Profiles And Scenarios

Certain situations almost always point you in one direction.

- The First-Time Home Buyer: If you’re new to the property game, it can feel like learning another language. A good mortgage broker is your best bet here. They act as a guide, translating the jargon, holding your hand through the paperwork, and saving you a mountain of stress. Plus, they shop around to find you a competitive deal when every single dollar makes a difference. Teaming one up with a professional like a buyers agent in Melbourne creates a powerhouse duo to get you into your first home with confidence.

- The Self-Employed Professional: Let’s be blunt: banks often see self-employed people as a risk because of fluctuating income. Walk straight into a bank, and you might get a swift ‘no’. A broker, on the other hand, knows exactly which lenders are more flexible with income verification. They’re experts at positioning your application to highlight your strengths, which massively boosts your chances of getting approved.

- The Seasoned Property Investor: An experienced investor rarely needs a simple, off-the-shelf home loan. They’re usually chasing specific products like interest-only loans, offset accounts, or complex financing across multiple properties. A broker’s access to a huge menu of products from dozens of lenders is absolutely essential for building a strategic and profitable portfolio.

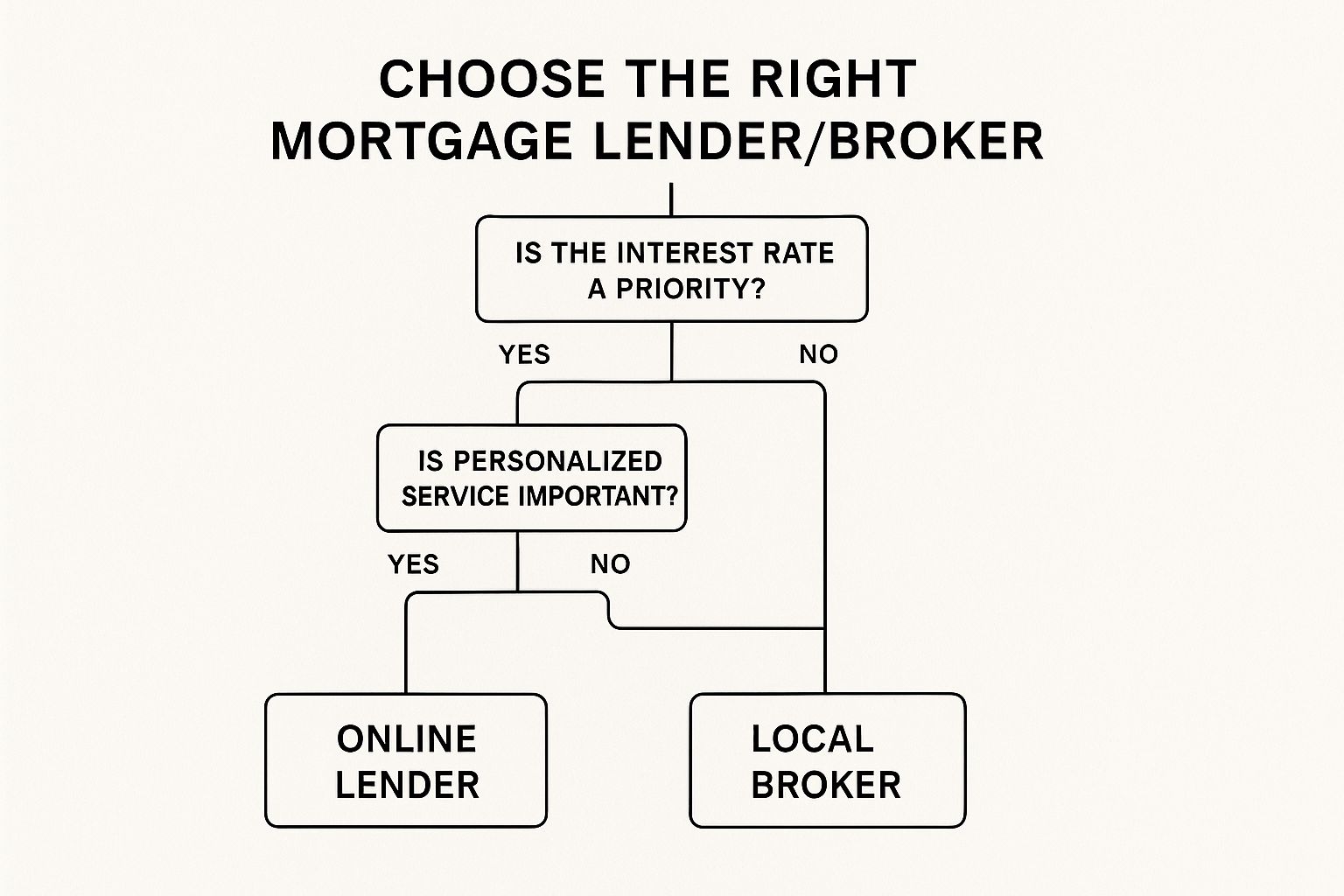

This quick visual guide can help you figure out which path lines up with what you value most.

As you can see, it often comes down to a simple trade-off: do you want the straightforwardness of dealing with one bank, or do you prefer having an expert navigate the entire market for you?

Scenario Guide Lender Vs Broker

To make it even clearer, this table breaks down a few more common borrower situations and which professional is likely the better fit.

| Borrower Profile | Recommended Path | Reasoning |

|---|---|---|

| Excellent Credit & Simple Finances | Direct Lender | With a straightforward application, you can often secure a competitive rate directly and save time. |

| Busy Professional, Time-Poor | Broker | A broker does all the legwork, from research to application, freeing up your valuable time. |

| Unique Property (e.g., Rural) | Broker | Brokers know which niche lenders are willing to finance non-standard properties that big banks might reject. |

| Credit History Issues | Broker | They have experience with specialist lenders who are more understanding of past credit blemishes. |

| Loyal Customer of a Big Bank | Direct Lender | You may be able to leverage your existing relationship for loyalty discounts or special offers. |

Ultimately, the best choice aligns with your financial complexity, confidence in the process, and how much time you’re willing to invest.

Market Trends Favour Brokers

The numbers don’t lie—Australians are voting with their feet, and they’re walking straight to brokers.

In the March 2025 quarter, mortgage brokers settled a record-breaking 76.8% of all new residential home loans in Australia.

This isn’t just a small shift; it’s a massive endorsement of the value brokers provide. It shows that in a complicated and often confusing market, most people prefer having an independent expert in their corner to compare all the options. With interest rates constantly changing, that expert advice is more critical than ever.

Industry insiders are now predicting that the broker market share could climb towards 80%, making them the undisputed go-to for Aussie home buyers.

How to Choose the Right Mortgage Professional

Okay, so you’ve figured out whether a lender or a broker is the right fit. That’s step one. Now for the most important part: picking the person who will guide you through one of the biggest financial moves you’ll ever make. This isn’t just about getting a loan; it’s about finding a partner you can actually trust.

Choosing the right professional means doing a bit of homework upfront. You need to vet your options properly to make sure you’re getting solid advice, transparent service, and a loan that genuinely works for you. The right mortgage lender or broker makes the whole process smooth. The wrong one? They can create a world of stress and cost you a fortune.

Your Vetting Checklist

Before you sign on the dotted line, you need to ask some hard questions. This is not the time to be shy—your financial future is literally on the line.

Here are the non-negotiables to ask any potential partner:

- For Brokers: How many lenders are on your panel? A bigger panel means more options for you. A broker with only a handful of lenders isn’t giving you much more choice than walking into a bank yourself.

- What are all the fees involved? Get a complete, line-by-line breakdown of every potential cost, from application fees to discharge fees down the track. Transparency is key.

- How will you communicate with me? Will it be regular emails, phone calls, or a client portal? It’s best to set clear expectations right from the start so you’re not left wondering what’s happening.

Spotting The Red Flags

Just as crucial as asking the right questions is knowing what warning signs to look out for. High-pressure sales tactics are a massive red flag. If you feel like you’re being rushed or pushed into a decision, walk away. Simple as that.

Any professional who isn’t completely upfront about their fees or commissions should be avoided. A trustworthy advisor will have no problem explaining exactly how they get paid for their services.

Other warning signs? A lack of clear licensing or credentials and a pattern of bad online reviews. While one grumpy customer isn’t a deal-breaker, consistent negative feedback is a serious concern. It’s also smart to choose a mortgage and finance broker who gets the digital world and has a solid, professional online presence.

Where to Find and Verify Professionals

Start by asking people you trust—friends, family, or even your real estate agent. A good old-fashioned word-of-mouth referral is often the most reliable way to find someone great.

Once you have a few names, it’s time to do your own digging:

- Check Their Licence: In Australia, every mortgage broker must hold an Australian Credit Licence (ACL) or be an authorised credit representative. You can easily verify this on the ASIC Connect Professional Registers.

- Read Recent Reviews: Look them up on Google and other independent sites. Pay close attention to how they respond to feedback, both good and bad. It tells you a lot about their professionalism.

- Conduct an Interview: Treat your first meeting like a job interview—because that’s what it is. You’re hiring them. See how well they know their stuff, assess their communication style, and most importantly, trust your gut. Do you feel comfortable with them?

So, How Do You Make the Final Call?

Alright, let’s land this plane. Choosing between a mortgage lender and a broker is a big deal, but it really doesn’t have to be a headache. By now, you get the fundamental difference: a lender sells you their home loans, while a broker shops the entire market to find the right one for you.

Your final decision really just boils down to what you value most.

Are you after the simple, familiar path of sticking with your own bank? Or do you want the wide-open choice and expert hand-holding that a broker brings to the table? There’s no single right answer here—just the one that feels right for your finances and your peace of mind.

A Quick Recap of the Key Factors

As you mull it over, keep these three things front and centre:

- Choice: A lender gives you a set menu. A broker opens up the whole buffet, with options from dozens of different lenders.

- Guidance: A broker is your personal guide through the entire maze. This is a game-changer, especially if you’re a first-home buyer or your financial situation is a bit tricky.

- Bargaining Power: Brokers often get access to wholesale rates the public can’t. They negotiate for a living, which could mean a better deal in your pocket.

The real goal here isn’t just to get a home loan; it’s to get the right home loan. One that sets you up for long-term financial success. Armed with what you now know, you’re in a great spot to pick a partner who can help you do just that.

Feeling clear and confident is the first step. The next is taking action.

That might mean booking a chat with your bank manager or starting your search for a well-regarded local broker. Whatever you choose, you’re now ready to make this decision without the guesswork.

Got Questions? We’ve Got Answers

Stepping into the world of home loans can feel like learning a new language. Let’s clear up some of the most common questions people have when trying to decide between a mortgage lender and a broker.

Does Using a Mortgage Broker Cost More?

This is probably the biggest myth out there. For most home loans, you don’t pay the mortgage broker for their service. It’s the other way around: the lender you end up choosing pays the broker a commission once your loan is finalised.

That fee isn’t tacked onto your loan, either. The interest rates and fees a broker can find are often the same, or even better, than what you’d get by walking into a bank yourself. Plus, safeguards like the Best Interests Duty in Australia mean brokers are legally bound to put your financial wellbeing ahead of their own commission cheque.

Can a Broker Really Get Me a Better Interest Rate?

More often than not, yes. Brokers have a couple of aces up their sleeve that can lead to a lower rate for you.

- Access to Wholesale Rates: Some lenders offer special, lower rates exclusively to brokers that aren’t available to the general public. Why? Because brokers bring them a steady stream of business, which saves the lender a fortune in marketing and sales costs.

- Negotiating Muscle: Brokers are in the trenches negotiating loans every single day. They know exactly how to position your application to get the most competitive deal and can even get lenders bidding against each other for your business.

While nothing’s guaranteed, their insider knowledge and access give you a much better shot at landing a great rate than going it alone.

What if I’m Not Happy With My Broker or Lender?

You’re never stuck. Whether you’re working with a direct lender or a broker, your rights as a consumer are well-protected, and there are clear steps you can take if you’re unhappy.

The best first move is always to raise the problem directly with the person or company. You’d be surprised how many issues get sorted out quickly through a simple conversation and their internal complaints process.

If that doesn’t get you a fair outcome, you can take it further. Every legitimate mortgage broker and lender in Australia must be a member of the Australian Financial Complaints Authority (AFCA). AFCA is a free, independent body that will investigate your complaint and help find a resolution.

This gives you a powerful ally and a formal process to follow, so you can have peace of mind right through your home loan journey.

Editorial Note

Homer Digital Marketing publishes practical guides on property marketing, digital visibility and lead generation strategies for service based businesses.